The report "Agricultural Packaging Market by Material (Plastic, Metal, Paper & Paperboard, Composites), Product (Pouches & Bags, Drums, Bottles & Cans), Barrier Strength (Low, Medium, High), Application, and Region - Global Forecast to 2023", The agricultural packaging market is projected to reach USD 5.02 Billion by 2023, from USD 3.93 Billion in 2018, at a CAGR of 5.00% during the forecast period. The market is driven by factors such as rising consumption of pesticides and fertilizers across the globe, increasing adoption of high barrier packaging materials for agrochemicals, increasing demand for extended shelf life of these products, and rising demand for biologicals across the globe owing to the increasing ban on chemical pesticides.

The years considered for the study are as follows:

Rigid plastics segment is estimated to be the most widely used material for agricultural packaging

Plastics are the most preferred packaging material used for pesticides and fertilizers, owing to the properties such as medium-barrier strength, cost-effectiveness, flexibility, and inertness. The packaging of chemical pesticides consumes a large amount of packaging material, when compared to fertilizers as fertilizers are usually packaged in larger volumes while pesticides are available across a wide volume range. Pesticides are majorly prepared in liquid formulation, which is most often packed in plastic bottles, cans, or containers. Rigid plastics such as HDPE are used for manufacturing such packaging solutions. Hence, the rigid plastics segment dominated the market share in plastics.

Medium-barrier strength segment is projected to be the fastest-growing during the forecast period

Medium-barrier strength materials such as plastics and some composites are widely used for packaging purposes across various industries, including agriculture. Their molding and low cost properties in comparison to other materials such as metals are the major reasons for the adoption of these materials by both the manufacturers and end use farmers on a wide scale. Composite materials are increasingly gaining interest among agrochemical manufacturers; however, the share of packaging in the agrochemical value chain is at a higher scale, when compared to plastic packaging. The demand for medium-barrier strength materials is expected to continue its dominance in next few years; hence, the segment is projected to grow at the highest rate during the forecast period.

Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=181856573

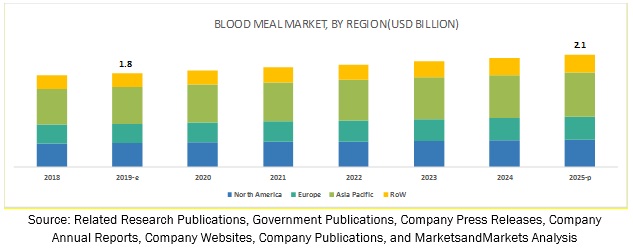

Asia Pacific is projected to dominate the market for agricultural packaging at the highest rate through 2023

Asia Pacific is the largest consumer of agricultural packaging owing to the large production capacities of agrochemicals prevailing in China and India, which makes it easier for most private, local companies to launch their products. The high labor power, fragmented packaging industry, and easy availability of packaging materials in Asia Pacific countries have resulted in significantly lower production costs. Additionally, factors such as growth in demand for biologicals, increase in trade opportunities of agrochemicals, and efficient infrastructure are the key competitive advantages for the Asia Pacific market.

The market for agricultural packaging in the Asia Pacific region is projected to grow at the highest CAGR of 6.17% from 2018 to 2023, owing to the increasing expansions of major agrochemical as well as agricultural packaging players in this market and growing demand for biologicals that has opened opportunities for the development of better packaging techniques in this industry.

This report includes a study of marketing and development strategies, along with the product portfolios of leading companies. It also includes the profiles of leading companies such as Amcor Limited (Australia), Bemis Company, Inc. (US), Sonoco Products Company (US), Grief Inc. (US), Mondi Group (South Africa), Packaging Corporation of America (US), NNZ Group (Netherlands), LC Packaging International BV (Netherlands), Silgan Holdings, Inc. (US), ProAmpac LLC (US), Flex-Pack (US), Purity Flexpack Limited (India), ePac Holdings LLC (US), Kenvos Biotech Co., Ltd. (China), and Parakh Group (India).

The years considered for the study are as follows:

- Base year – 2017

- Estimated year – 2018

- Projected year – 2023

- Forecast period – 2018 to 2023

- Determining and projecting the size of the agricultural packaging market, with respect to material, product, application, barrier strength, and regional markets, over a five-year period ranging from 2018 to 2023.

- Identifying attractive opportunities in the market by determining the largest and fastest-growing segments across regions.

- Analyzing the demand-side factors based on the impact of macro and microeconomic factors on the market and shifts in demand patterns across different subsegments and regions.

Rigid plastics segment is estimated to be the most widely used material for agricultural packaging

Plastics are the most preferred packaging material used for pesticides and fertilizers, owing to the properties such as medium-barrier strength, cost-effectiveness, flexibility, and inertness. The packaging of chemical pesticides consumes a large amount of packaging material, when compared to fertilizers as fertilizers are usually packaged in larger volumes while pesticides are available across a wide volume range. Pesticides are majorly prepared in liquid formulation, which is most often packed in plastic bottles, cans, or containers. Rigid plastics such as HDPE are used for manufacturing such packaging solutions. Hence, the rigid plastics segment dominated the market share in plastics.

Medium-barrier strength segment is projected to be the fastest-growing during the forecast period

Medium-barrier strength materials such as plastics and some composites are widely used for packaging purposes across various industries, including agriculture. Their molding and low cost properties in comparison to other materials such as metals are the major reasons for the adoption of these materials by both the manufacturers and end use farmers on a wide scale. Composite materials are increasingly gaining interest among agrochemical manufacturers; however, the share of packaging in the agrochemical value chain is at a higher scale, when compared to plastic packaging. The demand for medium-barrier strength materials is expected to continue its dominance in next few years; hence, the segment is projected to grow at the highest rate during the forecast period.

Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=181856573

Asia Pacific is projected to dominate the market for agricultural packaging at the highest rate through 2023

Asia Pacific is the largest consumer of agricultural packaging owing to the large production capacities of agrochemicals prevailing in China and India, which makes it easier for most private, local companies to launch their products. The high labor power, fragmented packaging industry, and easy availability of packaging materials in Asia Pacific countries have resulted in significantly lower production costs. Additionally, factors such as growth in demand for biologicals, increase in trade opportunities of agrochemicals, and efficient infrastructure are the key competitive advantages for the Asia Pacific market.

The market for agricultural packaging in the Asia Pacific region is projected to grow at the highest CAGR of 6.17% from 2018 to 2023, owing to the increasing expansions of major agrochemical as well as agricultural packaging players in this market and growing demand for biologicals that has opened opportunities for the development of better packaging techniques in this industry.

This report includes a study of marketing and development strategies, along with the product portfolios of leading companies. It also includes the profiles of leading companies such as Amcor Limited (Australia), Bemis Company, Inc. (US), Sonoco Products Company (US), Grief Inc. (US), Mondi Group (South Africa), Packaging Corporation of America (US), NNZ Group (Netherlands), LC Packaging International BV (Netherlands), Silgan Holdings, Inc. (US), ProAmpac LLC (US), Flex-Pack (US), Purity Flexpack Limited (India), ePac Holdings LLC (US), Kenvos Biotech Co., Ltd. (China), and Parakh Group (India).