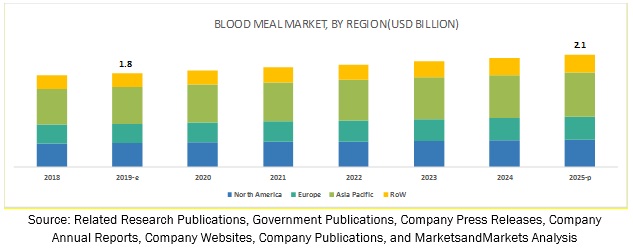

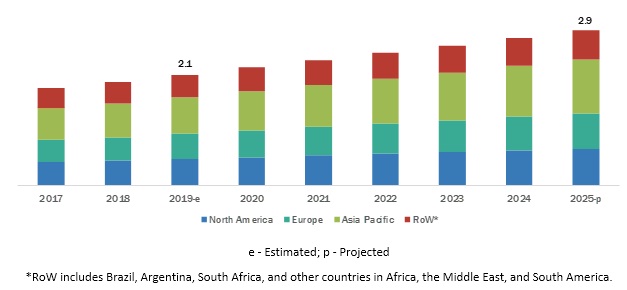

The report “Plasma Feed Market by Source (Porcine, Bovine, and Others), Application (Swine Feed, Pet Food, Aquafeed, and Others (Includes Ruminant and Poultry Feed)), Region (North America, Europe, Asia Pacific, and Rest of the World) – Global Forecast to 2025″ The plasma feed market is projected to reach USD 2.9 billion by 2025, from USD 2.1 billion in 2019, at a CAGR of 5.7% during the forecast period. The use of animal-derived plasma proteins as the replacement for antibiotics in feed drives the market for plasma feed.

Based on the source, the porcine segment is projected to be the larger contributor to the plasma feed market during the forecast period

The plasma feed market has been segmented, based on source, into porcine, bovine, and others, which includes sheep, goat, and poultry. The market for porcine plasma feed is projected to record a higher market share between 2019 and 2025. Porcine blood meal offers various health benefits to animals and is used significantly in poultry and porcine feed. For instance, as per the National Center for Biotechnology Information (NCBI), “pigs fed diets containing porcine plasma had greater average daily feed intake (ADFI) and average daily growth (ADG).”

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=205516339

Plasma feed is projected to be used majorly in pet food during the forecast period

The major factor for the higher adoption of plasma feed in pet food is anticipated because the tendency of people to humanize pets and treat them like their family members has resulted in the high demand for better quality pet food. The trend for the use of natural and bioactive products is very prevalent in the pet food industry. This is attributed to factors such as the expansion of the pet population, customer attitudes toward their pets as companions or family. As per Darling Ingredients, one of the major brand engaged in the production of plasma feed products quoted that plasma protein is a natural and sustainable source for pet food. It has several advantages such as water binding capacity, emulsifying properties, and palatability, which in turn drives the market for plasma feed among pet food manufacturers.

The Asia Pacific is projected to dominate the plasma feed market by 2025.

The Asia Pacific accounted for the largest share in the global plasma feed market for in 2018, and the market is projected to grow at the highest CAGR during the forecast period. China is the major reason for the dominance of Asia Pacific in the global plasma feed market, wherein China is one of the largest consumer and producer of overall meat products. China accounted for the highest share in the number of pigs slaughtered in 2017, which makes it the dominant market for porcine-based plasma feed. The Asia Pacific region is projected to be the fastest-growing market for the period considered for this study. The region’s growing concentration of animal slaughtering and increased demand for animal-based food products poses a strong potential for plasma feed manufacturers.

This report includes a study of the development strategies, along with the product portfolios of leading companies such as Darling Ingredients Inc. (US), The Lauridsen Group Inc. (US), SARIA Group (Germany), Sera Scandia (Denmark), Lican Food (Chile), Puretein Agri LLC. (US), Veos Group (Belgium), Kraeber & Co Gmbh (Germany), Rocky Mountain Biologicals (US), Lihme Protein Solutions (Denmark), EcooFeed LLC (US), and FeedWorks (Australia).

Critical questions the report answers:

- Where will all these developments take the industry in the mid-to-long term?

- What are the upcoming commercial prospects for the plasma feed market?

- What is the impact of high capital investment on the plasma feed market?

- What are the new technologies introduced in the plasma feed market?

- What are the latest trends in the plasma feed market?